The Great Digital Deception: How Global Chaos is Blinding Us to the Rise of State-Controlled Money

The Weekend Big Think

We are back team,

And we have a big one for you this weekend. Get your pots brewing and your finest robusta ground and prepare for a journey.

While the world's attention is captivated by escalating geopolitical tensions and economic turmoil in 2025, a far more insidious and transformative shift is occurring beneath the surface: the quiet ascent of stablecoins, which, under the guise of financial stability and efficiency, are inadvertently or perhaps purposefully paving the path towards a global, government-controlled monetary system capable of unprecedented citizen oversight and manipulation. This is not merely an economic evolution, but a profound redefinition of freedom and the very nature of sovereignty.

I. Opening Bell: Welcome to the Financial Funhouse

Alright, settle in, because we’re about to take a stroll through the financial funhouse, and let me tell you, some of the reflections in these mirrors are going to make you do a double-take. We are standing at the precipice of a financial revolution, and it’s not just about flashy apps or faster payments. Oh no, it’s about something far more fundamental: the very nature of money itself, and what it means for your individual financial autonomy and, dare I say, your peace of mind. Forget the quaint notion of a passbook savings account; a new game is unfolding, and its rules are being written in real-time.

The promise of a frictionless financial future is undeniably tantalizing. Instant transactions, global reach, and the potential to cut out those pesky intermediaries all sound like a dream, don't they? Like finding a twenty-dollar bill in an old coat pocket, but every single day. However, every dream casts shadows, and in this brave new digital world, those shadows are long, creeping, and potentially chilling. The subtle, and at times not-so-subtle, shift from convenience to control warrants a very close examination. The importance of a firm financial foundation and personal control over your money, often emphasized by folks like Dave Ramsey, takes on entirely new dimensions in this digital realm.

Consider the trajectory: the internet, once a novelty for simple communication, has rapidly evolved into the nervous system of our global financial lives. So, here’s the million-dollar question: what happens when this nervous system develops a mind of its own, or, more concerningly, when external forces begin to pull its strings? This article will delve into the digital currencies vying for dominance, the inherent human quirks that make us all a little vulnerable to financial pitfalls, and the intricate geopolitical chess game being played with your money as a central pawn.

It becomes clear that the very allure of seamless progress can, paradoxically, obscure a subtle but significant shift towards greater oversight. New financial technologies, such as stablecoins and Central Bank Digital Currencies (CBDCs), are consistently marketed based on their convenience, speed, and efficiency. And look, those benefits are indeed tangible and appealing to both users and businesses. Who doesn't love a faster transaction? But here’s the rub: the prioritization of immediate gratification, like transactional ease, can desensitize us to the underlying trade-offs, particularly concerning personal privacy and financial autonomy. This desensitization fosters an environment where greater centralized control, whether through programmable money or enhanced surveillance capabilities, can be introduced under the guise of "progress" or "security." The gradual erosion of individual financial freedom may then occur without widespread public outcry, akin to navigating a funhouse where familiar reflections become distorted, making it difficult to discern reality from illusion. You might just laugh all the way to the bank, only to find the bank is now watching your every move.

II. The Shiny New Toys: Stablecoins and the Global Money Race

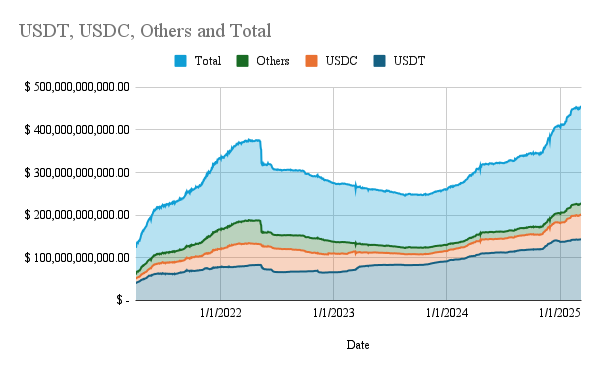

Suddenly, the financial world is abuzz with stablecoins. And the reason is straightforward: they promise the best of both worlds, combining the lightning speed and low cost typically associated with cryptocurrencies with the rock-solid stability of traditional fiat currency. Imagine sending $200 from the United States to Nigeria for less than a cent. For over a billion unbanked individuals globally, this isn't merely a convenience; it’s a potentially transformative development. This shift signifies that stablecoins are no longer solely a subject of speculative interest but are increasingly recognized for their strategic utility.

And boy, are the major players rapidly entering this arena.

PayPal, for instance, is making its PYUSD stablecoin available on the Stellar network, aiming for faster cross-border payments and micro-financing. They’re even looking at real-time wages in over 100 countries. Talk about a game-changer for your paycheck!

Stripe, a titan in payment processing, has launched "Stablecoin Financial Accounts," enabling businesses to hold balances in stablecoins, receive payments via both crypto and traditional fiat rails, and transfer stablecoins globally. They’ve even partnered with Visa for card-issuing products linked to stablecoin wallets, further bridging the digital and traditional financial worlds. When established financial giants like Visa and Mastercard are not just adopting these rails but actively building them, it signals a profound, structural investment in the digital future of money. We're talking about processing trillions of dollars in transactions, outpacing traditional networks.

However, this digital wild west is not without its sheriffs. Regulators are riding in to establish order, and they’re not messing around.

The U.S. Senate recently passed the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) with bipartisan support, aiming to create a unified and modern framework for dollar-backed stablecoins. This legislation mandates 1:1 reserve backing with high-quality liquid assets like U.S. currency and short-term Treasury bills, public disclosure of redemption policies, and strict compliance with Anti-Money Laundering (AML) and sanctions regulations.

Across the Atlantic, Europe's Markets in Crypto-Assets (MiCA) regulation is undertaking similar efforts, establishing a unified framework to address risks such as market abuse, financial instability, and consumer exploitation. These measures are designed to prevent the "bank-run" dynamics observed with some less-than-stable stablecoins.

Despite these regulatory advancements, the Bank for International Settlements (BIS), often referred to as the central bank to central banks, maintains a skeptical stance. The BIS argues that stablecoins fundamentally lack "singleness, elasticity, and integrity," classifying them as "unsound money." Concerns are raised about their potential to undermine monetary sovereignty through "dollarization" and to destabilize government debt markets if issuers were to sell off reserves en masse during crises. This represents a classic institutional pushback against private innovation, highlighting a fundamental tension in the evolving financial landscape.

The rapid adoption and utility of stablecoins, as evidenced by the involvement of major payment platforms, are undeniably significant. In response, regulators in the U.S. and Europe are implementing comprehensive frameworks to manage associated risks. While this regulatory intervention aims to enhance trust, reduce illicit activity, and generally foster mainstream adoption, it simultaneously introduces a complex trade-off. The stringent compliance requirements, particularly under MiCA, are increasing operational costs for crypto businesses, which in turn leads to market consolidation. This trend, while potentially boosting investor confidence by reducing fragmentation, may inadvertently stifle the very diversity and innovation that smaller, agile firms often bring to the market. The skepticism from institutions like the BIS further underscores a deeper dilemma: whether regulation is genuinely fostering innovation or primarily seeking to rein it in to protect existing monetary systems. This creates a paradox where efforts to legitimize stablecoins might inadvertently centralize them, making them more akin to traditional financial instruments and less aligned with the decentralized vision from which they emerged. This convergence could lead to a future where stablecoins, despite widespread adoption, function effectively as "franchisees of central banks," blurring the lines between private money and state control and potentially limiting their revolutionary potential in favor of systemic stability.

III. The Iron Fist in the Digital Glove: Central Bank Digital Currencies (CBDCs)

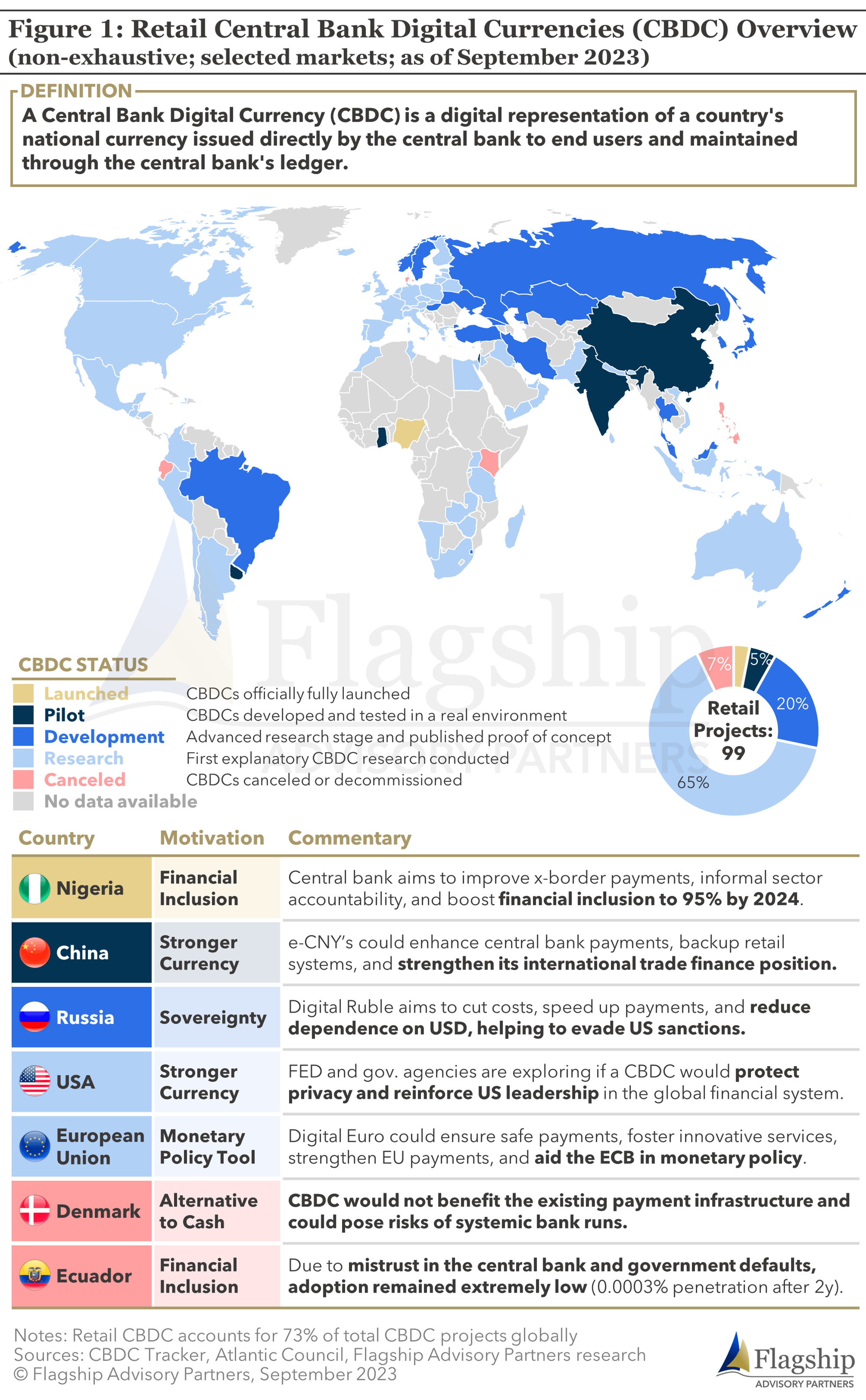

While private stablecoins are busy making waves and getting all the headlines, central banks are far from idle. Oh no, they are actively developing their own digital concoctions: Central Bank Digital Currencies, or CBDCs. Why this sudden governmental interest? Well, central banks recognize the undeniable march towards a cashless society and aim to maintain control over monetary policy, ensure financial stability, and promote financial inclusion. Approximately 94% of central banks globally are engaged in some form of CBDC development. Beyond the obvious efficiencies, such as reducing the costs associated with printing and distributing physical cash, the motivation for CBDCs runs far deeper. Because, let's be honest, who doesn't want to know exactly where every stimulus dollar goes? It's like trying to track a teenager's allowance, but with national security implications.

Leading this charge, as is often the case in digital innovation, is China. Its digital yuan, the e-CNY, is not merely digital cash; it embodies the concept of programmable money. Imagine a scenario where the government can essentially "tag" funds, imposing limitations or preconditions on their use. For instance, during periods of market shortages, individuals might find their e-CNY restricted to purchasing only certain quantities of scarce materials. Unlike money held in commercial banks, the e-CNY is a direct liability of the central bank. This design is not just about combating illicit activities; it is explicitly aimed at creating a "more intelligible and controllable economy." This capability suggests a level of financial oversight that extends beyond traditional monitoring, venturing into direct behavioral influence.

The e-CNY, when viewed in conjunction with China's already dominant digital payments landscape—where Alipay and WeChat Pay control an astounding 94% of mobile payments —and its controversial Social Credit System , paints a truly chilling picture. While Chinese authorities claim to offer "controllable anonymity" for small transactions , the underlying reality is the creation of a permanent, government-owned ledger where every transaction is recorded and traceable.

Reports have emerged of individuals being banned from mobile payments for "social credit" offenses, such as unpaid taxes or spreading "fake news," effectively stranding them in a cash-only world within a society that has largely abandoned physical currency. This punishment is described as "tantamount to social exclusion."

Picture old Mr. Li, a retired teacher in Shenzhen, who, after a lifetime of quiet obedience, finds his digital wallet frozen. Not for a financial crime, mind you, but because his social credit score dipped after his neighbor reported him for "spreading rumors" in an online chat group about local food prices. Suddenly, his QR code, once his passport to everything from groceries to bus rides, is useless. He's stranded, clutching a few crumpled yuan in a city that's forgotten cash, simply for speaking his mind. This is not a theoretical risk; it's a real-world consequence.

While some analyses suggest the e-CNY may not dethrone the U.S. dollar globally due to factors like capital controls and a lack of accessible assets , its domestic implications are profoundly significant. It functions as a tool for "unprecedented financial insight and real-time monetary and economic oversight" , potentially enabling the government to "seize digital wallets or stop payments" for those deemed to be in "political conflict" with the state.

The concept of "controllable anonymity" promoted by China for its e-CNY presents a fundamental paradox. While it suggests a balance between user privacy and government oversight for combating illicit activities, the very term "controllable" implies that anonymity is a conditional privilege, granted and revoked at the state's discretion. This means that the central bank retains the inherent ability to de-anonymize transactions at will. The e-CNY establishes a "permanent, government-owned ledger" where "every transaction is recorded and traceable." This capability, when combined with China's Social Credit System, allows for financial transactions to be directly linked to social and political behavior, leading to punitive measures such as bans from digital payments. This model sets a global precedent for "state-controlled financial surveillance." Even if other nations do not fully adopt such a system, the underlying concept of programmable and traceable money could spread, gradually eroding financial privacy worldwide. The concern extends beyond the citizens of China; it lies in the potential for any government to gain "enormous power over its citizens" through comprehensive financial data.

Furthermore, while China explicitly designed the e-CNY to challenge the U.S. dollar's global dominance and promote the internationalization of the Renminbi , its global impact remains limited. Technologically, the e-CNY offers instant, low-cost cross-border transactions, potentially surpassing existing systems like SWIFT. However, despite this technological sophistication, the e-CNY is effectively confined within the Chinese financial system due to persistent structural constraints, including stringent capital controls, underdeveloped financial markets, and a lack of robust rule-of-law safeguards. Foreign entities, for example, cannot easily reinvest their yuan earnings into profitable Chinese assets. This limitation in utility as a global reserve or trade currency demonstrates a crucial point: currency hegemony is not solely determined by technological prowess or governmental decree. It is fundamentally built upon trust, transparency, and the openness of a nation's financial markets and legal institutions. The very centralized control China seeks domestically, paradoxically, undermines its broader international ambitions. This serves as a significant lesson for any nation considering a CBDC: a closed, highly controlled system, regardless of its internal efficiency, will likely struggle to achieve widespread global acceptance.

IV. The Human Condition: Our Brains, Our Biases, Our Bucks

Alright, let's pull back the curtain on the true puppet masters of finance: our own squishy brains. Because no matter how advanced the technology becomes, humans remain, well, human. And emotions, particularly greed and fear, are notorious for transforming rational markets into a financial funhouse mirror.

Consider the infamous Tulipmania that gripped 17th-century Holland. People, driven by an insatiable hunger for more, mortgaged their homes for tulip bulbs, exchanging them for assets equivalent to oxen, sheep, and even an entire bed. Why? Pure, unadulterated greed. The prices soared, and everyone wanted a piece of the action. Until, of course, the bubble burst, leaving "hundreds who... had begun to doubt that there was such a thing as poverty... suddenly found themselves the possessors of a few bulbs, which nobody would buy." A similar narrative unfolded during the dot-com bubble of the late 1990s, where tech stocks skyrocketed on speculative fervor, only to plunge nearly 49% when the market corrected. This embodies the classic investment adage: "be fearful when others are greedy and greedy when others are fearful."

Then there's normalcy bias, the insidious little voice that whispers, "It will be fine. Things always go back to normal." This is the tendency to instinctively downplay the significance of potential threats, clinging to the comforting belief that life will follow a familiar course. This bias explains why investors often hold onto plummeting stocks, convinced they will "surely recover." It's also why individuals might dismiss warnings about the risks of new digital currencies, assuming, "Cash has always been king; it will never truly disappear." This cognitive bias fosters resistance to change and leaves individuals unprepared for significant disruptions.

Finally, the old crowd-pleaser: herd mentality. This is the irresistible urge to follow the actions of the majority, assuming that if everyone else is doing it, it must be the correct path. Observe a long line at a food truck, and the immediate thought is often, "Those must be good tacos." Witness a hot new stock being bought en masse, and the internal logic suggests, "One cannot go wrong, right?" This bias fuels market bubbles during periods of exuberance and triggers panic selling during downturns, as investors liquidate assets simply because others are doing so, often without independent analysis. Research indicates that as little as 5% of informed investors can influence the decisions of the remaining 95%. It is this collective psychological pull that causes individuals to be swept up in hype, whether it concerns tulips, tech stocks, or the latest digital currency.

The interplay of these behavioral biases fundamentally shapes financial vulnerability. Historical financial bubbles, such as Tulipmania and the Dot-com boom, were demonstrably driven by the powerful emotions of greed and fear. In contemporary financial decision-making, cognitive biases like normalcy bias and herd mentality continue to exert significant influence. These biases, individually, lead to irrational decisions, market volatility, and substantial individual losses. However, the true danger lies in their synergistic effect: the combination of these biases creates a self-reinforcing cycle of vulnerability. Normalcy bias prevents individuals from adequately preparing for radical shifts, such as the emergence of a cashless society or the widespread adoption of CBDCs. Simultaneously, herd mentality pushes individuals into speculative bubbles during periods of irrational exuberance or into panic selling during market downturns. Greed blinds individuals to risk during economic booms, while fear paralyzes them during busts. This "emotional roller coaster" is not merely a metaphor but a predictable pattern of human behavior within financial markets. This means that even with the most advanced financial technologies, the human element remains the most significant weak link. The most meticulously designed financial innovations can be undermined by the "delusions of crowds." Therefore, understanding these biases is not just an academic exercise; it is critical for personal financial survival and for making rational decisions in a rapidly evolving digital landscape.

To help you recognize these internal adversaries, here are some of your brain's worst enemies in finance:

Greed: An excessive desire for wealth or gain. Drives speculative bubbles; leads to irrational exuberance and taking on excessive risk in rising markets.

Fear: An unpleasant emotion caused by the belief that someone or something is dangerous, likely to cause pain, or a threat. Triggers panic selling; leads to irrational decisions to avoid losses, even if it means missing potential gains.

Normalcy Bias: The tendency to underestimate the likelihood or impact of a disaster or significant change. Causes inaction in the face of warning signs; leads to holding onto losing investments, assuming they will recover; resistance to adopting new, necessary behaviors.

Herd Mentality: The tendency to follow the actions of a larger group, often ignoring individual analysis. Fuels market bubbles and panic selling; leads to buying or selling assets simply because others are doing so, without independent research.

Confirmation Bias: Seeking out and interpreting information in a way that confirms one's existing beliefs. Ignoring red flags or contradictory evidence about an investment; rationalizing poor decisions.

Loss Aversion: The tendency to prefer avoiding losses over acquiring equivalent gains. Holding onto losing investments too long; selling winning investments too early; being overly conservative.

Overconfidence Bias: Overestimating one's own abilities, knowledge, or control. Making high-risk investments based on an inflated assessment of expertise; active trading with poor results.

Recency Bias: Over-relying on the most recent information or experiences, ignoring historical trends. Making investment decisions based solely on recent market performance, without considering long-term cycles.

V. The Cashless Conundrum: Losing Anonymity, Gaining Vulnerability

Remember physical cash? That crinkly paper or clinky metal that allowed for anonymous transactions, whether buying a coffee, paying for a haircut, or making a private donation without leaving a digital footprint? Well, it’s now undergoing a vanishing act. The undeniable shift towards digital payments is driven by compelling factors: convenience, efficiency, and a reduced risk of theft and money laundering. However, a critical question arises: what are we trading away for all this seamlessness?

Here lies the fundamental challenge: in a fully cashless system, every single transaction is recorded, stored, and traceable. Unlike cash payments, which offer inherent anonymity, digital methods leave a permanent electronic footprint. This extends beyond corporations tracking your spending for targeted advertisements, although that’s certainly occurring. It empowers governments with "enormous power over its citizens." The ability to monitor all economic activity raises profound concerns about a "techno-dystopian future" where a political dictatorship could suppress dissent more effectively. This pervasive loss of transactional anonymity represents a "major source of worry for civil rights."

The psychological implications of constant financial monitoring are also significant. Imagine the anxiety of knowing your spending is always being watched, leading you to adopt cautious spending behaviors out of fear of judgment, and feeling a decreased freedom in making spontaneous or private purchases. It’s enough to give you the chills.

Furthermore, it’s not only governments that wield this power. Private payment processors, the very companies facilitating your convenient digital life, hold immense influence. They can, and demonstrably do, act as arbiters of what speech and activities are deemed "acceptable."

Consider the heavy metal band Isis – formed years before the terrorist group. A fan, innocently buying a band T-shirt, found their payment suspended by PayPal.

Or the Muslim woman whose Venmo payment to a friend for dinner at "Al-Aqsa Restaurant" was flagged due to keywords.

These aren't just glitches; they're stark reminders that private companies, wielding immense power, can become arbiters of what's 'acceptable,' effectively silencing or inconveniencing individuals based on algorithms or external pressure. The implications are stark: imagine being advised to manage debt, only to find the system restricts essential purchases due to your online activities.

The transition to a cashless society, while offering undeniable convenience and efficiency , comes at a significant cost: the erosion of transactional anonymity. Every digital payment leaves a traceable footprint. This loss of anonymity directly enables pervasive financial surveillance by both corporations, for purposes of profiling and marketing, and governments, for control and suppression. This creates "information asymmetries" where powerful entities possess comprehensive data about individuals, while individuals have limited knowledge of how their data is being used. This power imbalance can lead to a "chilling effect" on behavior, prompting individuals to self-censor or alter their spending habits out of fear of judgment or control. The ultimate consequence is a significant erosion of personal freedom and autonomy. Financial tools, traditionally neutral mediums of exchange, risk becoming instruments of social engineering and control, blurring the lines between economic activity and political compliance. This represents a fundamental shift in the power dynamic between individuals and institutions, making the "cashless conundrum" a critical battleground for civil liberties.

Moreover, a society that relies entirely on digital systems and technology, as a cashless one inherently does , introduces a massive single point of failure. While this reliance can increase efficiency and reduce certain types of crime , it simultaneously decreases systemic resilience. System failures, cyberattacks, or even natural disasters could render entire financial systems useless, preventing individuals from accessing their money or purchasing essential goods and services. This is a direct trade-off: increased efficiency for decreased robustness. This vulnerability extends beyond mere technical glitches to encompass significant geopolitical risks. A nation heavily reliant on, for example, U.S.-based payment platforms could face "digital colonialism" or be severely impacted by escalating geopolitical tensions and currency competition. The disappearance of physical cash, therefore, is not just a domestic issue but also a national security concern, highlighting the imperative of diversifying beyond purely digital solutions for critical financial infrastructure.

VI. The Geopolitical Game: Money as a Weapon in a Fragmented World

Managing your personal finances can feel complicated enough, but imagine navigating the global economy in 2025. The world is characterized by "growing divisions," with "State-based armed conflict" identified as the top global risk. Wars are actively raging in Ukraine, the Middle East, and Sudan, creating a pervasive backdrop of instability that directly impacts global finance.

This is not merely background noise; it is a direct force shaping economic realities. "Geoeconomic confrontation"—a term encompassing sanctions, tariffs, and investment screening—has risen to become the third-highest global risk. The United States, for instance, is considering imposing tariffs of 60% on Chinese imports and up to 20% on all trading partners, a move that threatens to "upend the status quo and accelerate a rewiring of global trade flows." China, in turn, is tightening its control over its domestic economy and private sector. This is, in essence, financial warfare, and your individual wealth is often on the front lines. It's a global game of 'chicken,' only the chickens are entire economies, and the stakes are your retirement fund.

For decades, the U.S. dollar has reigned as the undisputed king of global finance, serving as the world's primary reserve currency. However, China's e-CNY, with its programmable features and cross-border ambitions, is explicitly designed to challenge this longstanding hegemony. Yet, as previously discussed, the e-CNY faces "old hurdles" such as stringent capital controls and a lack of accessible assets, suggesting it "won't dethrone the dollar" without major structural reforms to China's economic and legal frameworks. This situation presents a fascinating standoff: technological innovation confronting fundamental market principles.

In this increasingly digital and interconnected world, the risks extend beyond economic downturns or trade wars. They encompass the very digital infrastructure that underpins our global financial lives. "Cyber espionage and warfare" are now closely linked to state-based conflicts. A critical question arises: what would be the ramifications if a major payment network were crippled by an attack? Or if a central bank digital currency system were compromised? The BIS has warned that stablecoins could "destabilize government debt markets" if their issuers were to sell off reserves en masse during crises. The more digital global finance becomes, the more vulnerable it is to these systemic shocks.

The escalating geopolitical tensions, encompassing wars and trade disputes, are clearly manifesting as "geoeconomic confrontation" through sanctions, tariffs, and investment screening. This demonstrates a distinct trend of weaponizing financial systems. Money is no longer merely a medium of exchange; it has evolved into a potent tool of statecraft, utilized to exert influence, impose penalties on adversaries, and safeguard national interests. China's e-CNY, with its embedded surveillance and control capabilities, serves as a prime example of a currency designed with geopolitical leverage as a significant objective, even if its global adoption remains limited. The consequence is a "fragmented global economy" and increasingly complex supply chains, where financial decisions are progressively dictated by geopolitical alignments rather than purely economic efficiency. This implies that individual investors and businesses must now navigate a landscape where their financial stability is inextricably linked to global political stability, elevating "personal finance" to a matter requiring "geopolitical literacy."

Furthermore, the rapid advancements in digital currencies, including stablecoins and CBDCs, alongside the proliferation of artificial intelligence, represent a major technological transformation. While these technologies offer significant economic advantages and efficiencies, the pursuit of technological dominance, particularly in AI and digital finance, has become a critical component of national security and global influence. This dynamic has initiated a "digital arms race," where cyber warfare and espionage pose critical risks. The impetus behind the development of CBDCs, for instance, is partly driven by a desire to "keep pace with new fintech concepts like stablecoins" and to ensure "financial sovereignty." This suggests that the future of money is not only about financial innovation but also about securing critical digital infrastructure against state-sponsored attacks. The stability of your digital wallet could, in the future, directly depend on the geopolitical stability of the world, adding a layer of existential risk to everyday financial transactions.

VII. Your Financial Freedom: Navigating the Digital Wilds

Enough with the potential pitfalls and global chess matches; it’s time to focus on actionable strategies for you. The principles of financial control and a solid foundation, often championed by folks like Dave Ramsey, are more critical than ever in this digital age.

Here’s how you can take the reins:

Tackle that debt, digital or otherwise. Monthly payments on debt tie up your most important wealth-building tool: your income. Whether it’s credit card debt or a loan taken for a new crypto venture, it remains a drain on your resources. Prioritizing debt elimination frees up capital for more productive uses. Get mad at that debt and crush it!

Build a robust emergency fund. Just as 3-6 months of living expenses are recommended in easily accessible funds for life's unexpected events , preparedness for digital disruptions is equally vital. What if your preferred payment app experiences an outage? What if a cyberattack freezes accounts? Maintaining some physical cash and diversifying digital holdings across reputable, regulated platforms can provide crucial resilience. Don't be caught with your digital pants down!

Invest wisely and deliberately, not emotionally. The behavioral biases we just talked about—greed, fear, normalcy bias, and herd mentality—can easily derail sound financial decisions. Do not let these emotions drive your investment choices. Consistent investment in good growth stock mutual funds, maintaining a long-term perspective, remains a foundational strategy. Chasing the latest digital fad simply because it's popular can lead to significant losses. Collaborating with a financial advisor can provide an objective perspective, helping you make rational decisions rather than succumbing to emotional impulses.

Beyond these foundational principles, a discerning approach to new financial technologies is essential. It’s prudent to maintain a healthy skepticism and to understand the underlying mechanisms of financial systems, rather than simply accepting headlines. When confronted with new financial "innovations," a critical eye is necessary. For instance, any promise of "12 percent returns with no risk of loss from trading foreign exchange" should immediately trigger alarm, as such guarantees almost invariably indicate fraudulent activity. This principle extends to anything in the digital realm that appears too good to be true.

Furthermore, understanding the "plumbing" of digital currencies is crucial. It’s not enough to simply use a digital currency; you must comprehend how it operates, who controls it, and what data it collects. Is it a CBDC offering "controllable anonymity" , or a stablecoin backed by audited reserves? The critical details often reside in the fine print. By understanding the inherent absurdities and complexities of finance, you can better position yourself to identify genuine opportunities and avoid common pitfalls. The timeless wisdom of being fearful when others are greedy and greedy when others are fearful remains highly relevant.

To navigate these digital wilds effectively, here are some actionable recommendations:

Diversify, Diversify, Diversify: This applies not only to investments but also to payment methods. Avoid placing all financial reliance on a single digital basket. Maintain multiple accounts, utilize different payment applications, and, crucially, retain some physical cash.

Practice Digital Hygiene: Implement robust cybersecurity measures, including strong, unique passwords and two-factor authentication. Exercise extreme caution regarding phishing scams and suspicious digital communications. Your digital wallets and financial accounts are prime targets for malicious actors.

Advocate for Privacy: Recognize that convenience frequently comes at the cost of privacy. Actively support policies and technologies that prioritize user data protection and financial anonymity. Your freedom depends on it.

Read the Fine Print: Before adopting new digital financial products, thoroughly review the terms of service, redemption policies, and data collection practices. Understanding these details is critical for protecting your personal financial interests and autonomy.

The evolving digital finance landscape necessitates a blended approach to financial resilience, marrying prudence with skepticism. Traditional financial principles, emphasizing debt elimination, emergency funds, and long-term investing , provide the foundational stability required to weather inevitable market and technological shocks, thereby preventing catastrophic losses. Concurrently, a skeptical mindset, encouraging a deep understanding of market mechanics and the ability to discern genuine innovation from speculative hype , equips you to analyze complex and potentially deceptive financial innovations, protecting you from becoming unwitting victims. This synthesis of approaches prevents both naive optimism, which can lead to overexposure to risk, and paralyzing fear, which can prevent participation in legitimate growth opportunities. True "financial freedom" in the digital age, therefore, is not merely about accumulating wealth; it is about building resilience against systemic risks and maintaining autonomy in a world increasingly moving towards centralized control. It involves being both financially astute and digitally vigilant, actively participating in shaping your financial future rather than passively accepting what is presented.

VIII. Final Thoughts: The Unwritten Chapter of Your Financial Future

So, there it is. We’ve explored the fascinating, often absurd, world of financial engineering, smiled at the sheer promise of technological innovation, and perhaps, just perhaps, felt a shiver down the spine contemplating the creeping shadows of control. The digital dollar dilemma is not a distant problem; it is here, now, actively shaping the very fabric of your financial life.

The future of money is not a foregone conclusion. It is an unwritten chapter, and you, as the reader, are holding the pen.

Will it unfold into a future of unprecedented convenience and prosperity, or one of pervasive surveillance and stifled freedom? The choices you make, the questions you ask, and the vigilance you maintain will collectively determine the final draft. Stay informed, remain skeptical, and, most importantly, preserve your personal financial freedom in this evolving landscape. Because in the end, your money, your rules.

Or at least, they should be.