The Shadow Portfolio: Every Position Is a Confession

An Introduction to Your Financial Unconscious

Happy Saturday,

Time to open up your mind once again!

There is a moment, familiar to anyone with a brokerage account, that is one of the most psychologically revealing acts of modern life. It is the moment you open the app. Before the numbers resolve, before you see the day’s change in dollars or percentages, you feel something. A hum of anticipation. A knot of dread. A flicker of hope. It is a feeling that comes from a place far deeper than your rational analysis of market conditions. It is your unconscious, waving from the psychic basement, trying to get your attention.

That screen, with its tidy rows of tickers and flashing green and red lights, is not just a statement of assets. It is a confession booth where you use symbols instead of words. It is a diary written in the language of capital allocation. It is a meticulously curated museum of your anxieties. Every trade is a therapy session, and every portfolio is a diagnosis.

Enter Carl Jung, the Swiss psychiatrist who, it turns out, might have been the world’s first and best behavioral economist. Long before academics started documenting cognitive biases with Greek letters, Jung was mapping the strange, irrational territory of the human mind. His most potent concept for our purposes is the “Shadow.” The Shadow is the archetypal figure that lives in the unconscious, a psychic container where we shove all the parts of ourselves we find unpleasant, shameful, or socially unacceptable. It is, in Jung’s memorable phrasing, “the thing a person has no wish to be”. Your aggression, your fears, your immoral urges, your unfulfilled desires all the messy stuff that clashes with the polished version of yourself you present to the world gets repressed into this cellar.

But the Shadow does not simply lie dormant. When ignored by the conscious Ego, it has a way of making itself known. It acts out. It projects itself onto the world, seeking the attention it’s been denied. And what is a portfolio if not a grand, capital-intensive projection of the self onto the world of financial markets? Jung offered a warning that could be engraved on the door of every trading floor: “Until you make the unconscious conscious, it will direct your life and you will call it fate”. Rephrased for the modern investor, it might read: Until you understand the real reasons you own what you own, your portfolio will be managed by a panicky goblin in your subconscious, and you will call it ‘market conditions’.

This may sound more mystical than financial, but it provides a compelling narrative for the otherwise sterile observations of behavioral finance.¹ The well-documented menagerie of cognitive biases—loss aversion, confirmation bias, herd mentality—are just the scientific labels for the observable tantrums of an unacknowledged Shadow. Behavioral finance meticulously describes what happens when investors act irrationally: they sell winners too soon and hold losers too long (the disposition effect), they seek out information that confirms their existing beliefs, and they follow the crowd into bubbles and out of crashes.

These are the symptoms. Jung’s theory of the Shadow offers a story about the underlying disease. It suggests that the irrationality isn’t a bug in the system; it’s a feature of a psyche at war with itself, a "house divided". The market, then, becomes the stage upon which this internal drama plays out, with real money at stake.

The Technoking's Shadow and the Fear of Being a Dinosaur

Consider the tech-heavy portfolio, a shrine to innovation and forward-thinking. The persona of the tech investor is that of a visionary, a person who gets the future. Their conscious identity is aligned with progress, disruption, and the exponential curves of technological advancement. They are long artificial intelligence, quantum computing, and whatever sci-fi concept is currently being pitched in a seed round. Their ego is confident, forward-looking, and utterly convinced it’s on the right side of history.

But what is being repressed? What lives in the Shadow? The Shadow-self of the tech bull is the part of them that feels old, slow, and terrified of being left behind. It is the part that remembers Blockbuster Video with a shudder, not of nostalgia, but of existential dread at the thought of becoming it. Every long position in a disruptive technology company is a desperate attempt to silence the Shadow’s panicked whisper: “You are becoming obsolete.”

This isn’t just the fear of missing out on financial returns, a simple case of FOMO. It is a deeper terror of waking up one day to find the world has moved on, rendering one’s skills and worldview irrelevant. This anxiety is not just personal; it's corporate. In their annual 10-K filings with the SEC, companies now include detailed risk factors about AI. These are not just boilerplate legal disclosures; they are corporate confessions on paper. A company might disclose that AI could "make older products and offerings obsolete faster" or that failing to keep up with AI could harm their "strategy, productivity, competition or product demand". This is the collective, institutional expression of the exact same fear of irrelevance that drives the individual investor.

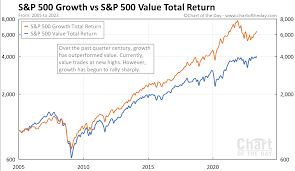

This psychological dynamic helps explain one of the most enduring puzzles in finance: why "growth stocks" are so often overvalued. For nearly a century, investors have consistently paid a premium for companies with high growth prospects, resulting in systematically lower long-term returns compared to boring "value" stocks.

Research from the Kellogg School suggests that overpaying for growth stocks can be seen as a rational act of purchasing insurance. When a disruptive innovation appears, it creates unpredictable winners and losers through "creative destruction." Investing in a company like Tesla, even at a steep valuation, becomes a hedge against being on the losing side of that disruption—an insurance policy against being left behind in the "Technochasm," the widening wealth gap driven by technology.

The investor cannot easily control their own professional obsolescence, but they can control their portfolio. They project their internal fear of becoming a fossil onto the external marketplace and attempt to solve it there by buying the future. A hypothetical conversation between a tech investor and their Shadow might go something like this:

Investor’s Ego: "I'm investing in DeepSeek because it's redefining the benchmark for legacy AI and disrupting entire sectors!"

Investor’s Shadow: (Whispering) “…and because you still aren’t 100% sure how to use TikTok and it makes you feel like a dinosaur whose asteroid is already in the atmosphere.”

In Code We Trust (Because We Don't Trust Anything Else)

Next, one finds the portfolio of the gold bug and the Bitcoin maximalist. The conscious persona here is that of a clear-eyed realist who understands the fatal flaw of fiat currency: it is designed to lose value over time. Central banks target inflation, and governments print money, systematically debasing the currency. Holding gold or Bitcoin is presented as a rational escape, a way to be one’s own bank by holding a "bearer asset" with a capped supply, free from the whims of unaccountable policymakers.

Here, however, is where it gets interesting. Empirical research throws a wrench into this self-conception. A study using representative data from the U.S. Survey of Consumer Payment Choice found that, contrary to the popular narrative, cryptocurrency investors show no more distrust in fiat currencies or regulated banks than the general population. They are not, as a group, financial anarchists fleeing a collapsing system.

So, what is the Shadow up to? One possibility is that the real motivation is pure speculation. The crypto market is a global casino that never closes, offering volatility and the potential for life-changing gains. The "distrust" narrative becomes a convenient, high-minded justification for the Shadow's more primal desire for the thrill of high-stakes gambling.

The persona wants to be a monetary dissident; the Shadow just wants to go to Vegas. This is most visible not in Bitcoin, but in the bizarre menagerie of altcoins. Consider a project like "Wall Street Pepe ($WEPE)," a meme coin whose mascot is a cartoon frog in an analyst's suit, with the stated goal of empowering "small investors to take action and beat whales at their own game". Or "Solaxy ($SOLX)," which features a mascot that is a "mash-up of Pepe and Einstein" and aims to solve Solana's network issues. The conscious mind claims it's building a new financial system; the Shadow is busy merging cartoon frogs with German physicists. This is not a coherent monetary philosophy; it's the id having fun with a blockchain.

The ultimate confession, the tell-tale sign of this internal conflict, comes from the existence of stablecoins. In a universe supposedly built on the rejection of centralized fiat, the safest and most functional corners are digital tokens that achieve stability by… pegging themselves to the U.S. dollar. This act of "piggybacking on the credibility provided by the central bank" is a beautiful, unconscious admission that the Shadow secretly craves the stability of the very system the ego claims to reject.

The ESG Guilt Offset

The rise of Environmental, Social, and Governance (ESG) investing represents one of the most sophisticated psychological maneuvers in modern finance. It can be understood as a form of psychic carbon offsetting—a mechanism for managing the guilt that comes from participating in a morally complex capitalist system.

Its predecessor, Socially Responsible Investing (SRI), was explicitly about values, often using negative screens to exclude "sin" stocks. Modern ESG, however, has been ingeniously reframed from being values-based to value-based. The central argument is not that it is the right thing to do, but that it is the profitable thing to do.

This reframing has been wildly successful, but it has created a profound disconnect. While the industry talks about risk management, surveys show that most retail investors still believe ESG investing is a way to "make positive change in the world". They are buying a product they believe is about expressing their values.

Herein lies the Shadow’s dirty secret. A devastating critique of the ESG-industrial complex reveals that most ESG rating frameworks do not actually measure a company's harm to the world; they measure the world's potential harm to the company's shareholders. It’s not about preventing the oil spill; it’s about making sure the oil spill doesn’t create a public relations nightmare that tanks your investment.

To see this in action, look no further than the Unusual Whales Subversive Democratic Trading ETF (ticker: NANC). This is a thematic ETF designed to invest in the stocks purchased by Democratic members of Congress. The psychological premise is fascinating—it's a bet on the political alignment and, implicitly, the informational advantage of a specific political tribe. But a peek under the hood reveals the beautiful contradictions the Shadow loves.

The fund's top holdings include tech giants like NVIDIA and Microsoft, consumer cyclicals like Amazon, and even Philip Morris International, a tobacco company. An investor might buy this fund with the conscious persona of aligning their capital with a political ideology, while their Shadow is quietly getting exposure to Big Tech and Big Tobacco. The ESG label, in its broadest sense, allows the investor to feel virtuous while the portfolio does what portfolios have always done: seek returns across the complex and morally gray landscape of the public markets.

The investor’s persona is that of the "conscious capitalist." The Shadow is the part of the self that feels a vague guilt about its own consumption and its complicity in a system that generates pollution and inequality. The ESG fund becomes a perfect mechanism to launder this guilt, offering the feeling of doing good while promising to enhance financial returns.

Confessions from the Rest of the Asylum

Before we psychoanalyze the final inmates, we must draw a distinction. Jung identified two layers of the unconscious. The personal shadow is ours alone—the fears and failings we repress from our own life experiences. But there is also a collective shadow, which contains the repressed darkness of an entire group or culture. The following archetypes reveal both.

The Value Investor: Fear of Being the Fool

The persona of the value investor is the epitome of rationality. They are the sober adult in a room full of speculators. They pore over balance sheets and demand a "margin of safety." Their mantra, from Warren Buffett, is to be "fearful when others are greedy and greedy only when others are fearful". But what is the Shadow of this hyper-rational being? It is a deep, abiding terror of being played for a fool.

Their entire methodology is an intellectual fortress built to defend against the psychic pain of being the "greater fool"—the patsy left holding the bag when the bubble pops. The "greater fool theory" posits that you can profit from an overvalued asset as long as you can sell it to an even "greater fool". The value investor's every calculation is a ritual to ensure that when the music stops, they are not the one left holding the worthless asset. Their fear is not of losing money, but of losing money in a way that proves they were stupid.

The Boglehead: Fear of Being Wrong

The persona of the Boglehead, the passive index fund investor, is one of transcendent wisdom. They buy the entire market through low-cost index funds, set it, and forget it. Their conscious persona is correct: the data overwhelmingly supports passive investing. Their strategy is the epitome of rationality. But the emotional appeal of this rationality, the deep comfort it provides, comes from the Shadow.

The Shadow is not afraid of being illogical; it is terrified of the regret and personal accountability that comes from making an active choice and having it blow up. The Boglehead three-fund portfolio is the ultimate abdication of choice. By buying the whole haystack, they never have to face the soul-crushing regret of having picked the wrong needle. If the portfolio goes down, it is not their fault; it is the market’s fault. It is a confession of a repressed desire to escape the anxiety of personal responsibility.

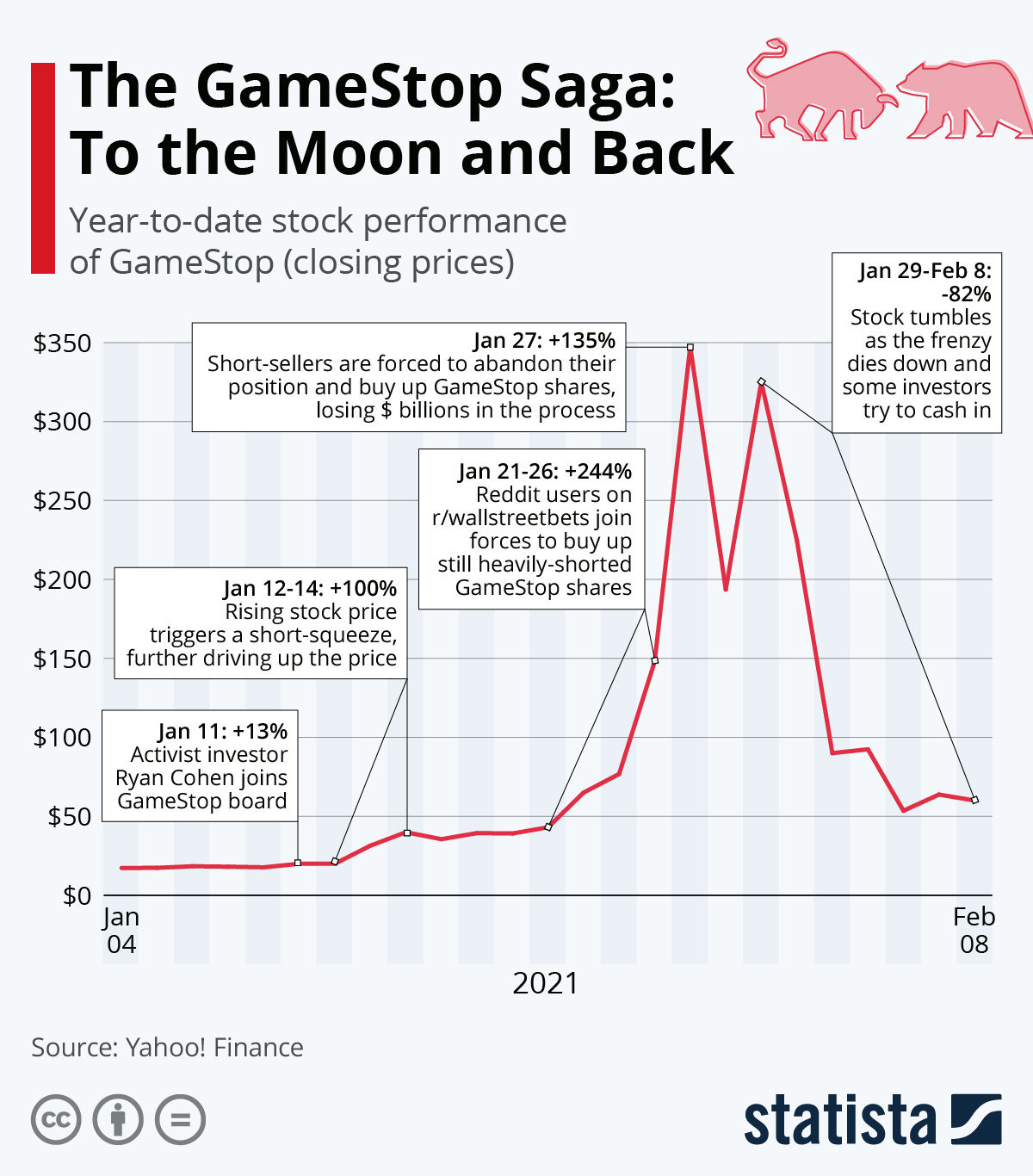

The Meme Stock "Ape": The Collective Shadow Unleashed

The GameStop saga of 2021 was not an investment strategy; it was the eruption of the collective Shadow. For years, a narrative of a rigged financial system had simmered, a feeling among many that Wall Street operated by a different set of rules, particularly after the 2008 financial crisis. This repressed rage found its outlet in GameStop. The persona of Wall Street is one of sophistication and professionalism. The meme stock traders on WallStreetBets adopted the opposite identity, embracing the Shadow by calling themselves "apes," "degenerates," and "retards". This was a deliberate inversion of the dominant culture.

The explicit motivation was a revenge fantasy, a chance for the "little guy" to inflict massive losses on the hedge funds that had shorted the stock. This was the collective Shadow, ignored for too long, finally grabbing the wheel of the car. It was not finance; it was catharsis.

From Confession to Conversation: On Shadow Integration

To apply a psychoanalytic lens to financial markets is to speak in metaphor. This is not a scientific model for portfolio construction. There is no "Shadow-Adjusted Return" metric to optimize.

But it is a useful story. It is a lens that reveals truths about motivation that a discounted cash flow model will always miss. The point of this exercise is not to exorcise the demon. Jung’s goal was never to eliminate the Shadow, which he considered impossible, but to integrate it. The process is about making the unconscious conscious, turning a confession into a conversation.

Acknowledging that a tech-heavy portfolio might be driven by a fear of obsolescence does not mean one should sell all their Nvidia stock. It means one can now ask a better question: "Am I holding this based on a sound analysis, or is my inner dinosaur panic-buying a ticket on the spaceship?" Recognizing that an ESG fund might be more about assuaging guilt than saving the planet allows for a more honest assessment: "Am I seeking to make a real-world impact, or am I just paying for moral indulgence?"

This is the practice of "shadow integration": a gradual, ongoing process of turning the unconscious monologue of your portfolio into a conscious dialogue with yourself. It transforms the portfolio from a mere tool for wealth creation into a powerful diagnostic tool for self-knowledge. Managing money becomes a path to managing the self. It is the difference between your portfolio being your fate, and it being your choice.

The analysis leaves not with answers, but with a new set of questions. They are not comfortable questions, but they are perhaps the most important ones an investor can ask.

Look at your largest holding. Is it a bet on the future, or an insurance policy against your deepest fear?

If your portfolio could speak, what would it confess about you? What part of yourself have you outsourced to the market to manage?

Are you investing for the person you are, or for the person your Shadow is terrified of becoming?

What if the most important form of diversification isn’t across asset classes, but across your own internal conflicts?

Of course, applying a psychoanalytic lens to markets is an exercise in metaphor, not econometrics. Psychoanalytic theories are notoriously difficult to quantify and have faced valid criticism for their isolation from empirical science. We are not building a predictive model here; we are telling a story. But sometimes, a story is the best way to understand a truth that a spreadsheet cannot capture.